![]()

Get instant access to FAR Practice Tests 2025 Free Updated Today!

Welcome to download the newest PassLeader FAR PDF dumps ( 165 Q&As)

Topics of Financial Accounting and Reporting (FAR) Exam

The syllabus for the Financial Accounting and Reporting (FAR) part of the Certified Public Accountant (CPA) Exam can be found in the FAR exam dumps and is also listed below with detail of each area of concern and their topics:

Area 1 - Conceptual Framework, Standard-Setting and Financial Reporting (25-35%)

Objectives covered by this section:

- Public company reporting topics (U.S. SEC reporting requirements, earnings per share, and segment reporting)

- Discontinued operations

- Financial statements of employee benefit plans

- Income statement/ statement of profit or loss

- Conceptual framework and standard-setting for business and non-business entities

- Statement of financial position

- General-purpose financial statements: for-profit business entities

- Notes to financial statements

- Balance sheet/ statement of financial position

- Statement of changes in equity

- Going concerned

Area 2 - Select Financial Statement Accounts (30-40%)

Objectives covered by this section:

- Debt covenant compliance

- Income taxes

- Long-term debt (financial liabilities)

- Financial assets at amortized cost

- Property, plant, and equipment

- Financial assets at fair value

- Notes and bonds payable

- Investments

- Trade receivables

- Equity

- Retirement benefits

- Intangible assets - goodwill and other

- Stock compensation (share-based payments)

- Payables and accrued liabilities

Area 3 - Select Transactions (20-30%)

Objectives covered by this section:

- Software costs

- Contingencies and commitments

- Derivatives and hedge accounting (e.g. swaps, options, forwards)

- Business combinations

- Subsequent events

- Research and development costs

Area IV - State and Local Governments (5-15%)

Objectives covered by this section:

- Expenditures and expenses

- Budgetary accounting and encumbrances

- Governmental funds financial statements

- General and proprietary long-term liabilities

- Budgetary comparison reporting

- Typical items and specific types of transactions and events: measurement, valuation, calculation, and presentation in governmental entity financial statements

- Capital assets and infrastructure assets

- Fund balances and components thereof

- Management's discussion and analysis

- Nonexchange revenue transactions

- Proprietary funds financial statement

How to Prepare For Financial Accounting and Reporting (FAR) Exam

Preparation Guide for Financial Accounting and Reporting (FAR) Exam

Introduction

The Financial Accounting and Reporting FAR exam test is part of the uniform CPA examination and is administered by the American Institute of Certified Public Accountants (AICPA). The American Institute of Certified Public Accountants (AICPA) is the United States national professional association of Certified Public Accountants (CPAs), with more than 418,000 members in business and industry, public practice, government, education, student affiliates, and foreign associates in 143 countries. Established in 1887, the association sets ethical guidelines for audits of private businesses, non-profit organizations, federal, state, and local governments for the profession and U.S. auditing standards. It also establishes the Standardized CPA Test and rates it. The AICPA has offices in New York City; Durham, NC; Washington DC; and Ewing, NJ.

For practitioners aspiring to become CPAs, the Standardized Certified Public Accountant test is a credentialing exam. It is graded and governed by the American Institute of Certified Public Accountants (AICPA) and by the National Association of State Accountancy Boards (NASBA).

This exam guide is intended to get you to know about the exam details and help you to prepare for the Financial Accounting and Reporting FAR exam test successfully. This guide includes information on the certification test target audience, recommended preparation FAR exam dumps and documentation, and a full list of exam targets, all to help you obtain a passing grade. To increase your chances of passing the test, AICPA strongly recommends a mix of on-the-job experience, course attendance, and self-study.

NEW QUESTION # 71

Which of the following factors determines whether an identified segment of an enterprise should be

reported in the enterprise's financial statements under SFAS No. 131, Disclosures about Segments of an

Enterprise and Related Information?

I. The segment's assets constitute more than 10% of the combined assets of all operating segments.

II. The segment's liabilities constitute more than 10% of the combined liabilities of all operating segments.

- A. Both I and II.

- B. II only.

- C. I only.

- D. Neither I nor II.

Answer: C

Explanation:

Choice "a" is correct. For segment reporting, if an identified segment's assets constitute more than 10% of

the combined assets of all operating segments, the segment should be reported. The same rule does not

apply for the segment's liabilities. The candidate does have to remember the 10% and also the 10% of

"what." Choice "b" is incorrect. For segment reporting, if an identified segment's assets constitute more

than 10% of the combined assets of all operating segments, the segment should be reported. The same

rule does not apply for the segment's liabilities. Choice "c" is incorrect. For segment reporting, if an

identified segment's assets constitute more than 10% of the combined assets of all operating segments,

the segment should be reported. The same rule does not apply for the segment's liabilities, so the correct

answer cannot be "Both." Choice "d" is incorrect. For segment reporting, if an identified segment's assets

constitute more than 10% of the combined assets of all operating segments, the segment should be

reported. The correct answer cannot be "Neither."

NEW QUESTION # 72

In the hierarchy of generally accepted accounting principles, APB Opinions have the same authority as

AICPA:

- A. Issues Papers.

- B. Accounting Research Bulletins.

- C. Statements of Position.

- D. Industry Audit and Accounting Guides.

Answer: B

Explanation:

Choice "d" is correct. AICPA Accounting Research Bulletins, FASB Standards, FASB Interpretations,

FASB Staff Positions, FASB Statement 133 Implementation Issues, and APB Opinions and

Interpretations are the most authoritative sources of generally accepted accounting principles. Choice "a"

is incorrect. AICPA Statements of Position, AICPA Accounting and Auditing Guides, and FASB Technical

Bulletins are secondary sources of generally accepted accounting principles. Choice "b" is incorrect.

AICPA Statements of Position, AICPA Accounting and Auditing Guides, and FASB Technical Bulletins

are secondary sources of generally accepted accounting principles. Choice "c" is incorrect. AICPA Issues

Papers and Practice Bulletins, FASB Concepts Statements, and other authoritative pronouncements are

tertiary sources for generally accepted accounting principles.

NEW QUESTION # 73

Which of the following statements regarding fair value is/are correct?

I. The fair value of an asset or liability is specific to the entity making the fair value measurement.

II. Fair value is the price to acquire an asset or assume a liability.

III. Fair value includes transportation costs, but not transaction costs.

IV. The price in the principal market for an asset or liability will be the fair value measurement.

- A. I & IV

- B. II & III

- C. I & II

- D. III & IV

Answer: D

Explanation:

Choice "d" is correct. Statements III and IV are correct. Statement I is incorrect because fair value is a

market-specific measure, not an entity-specific measure. Statement II is incorrect because fair value is an

exit price (the price to sell an asset or transfer a liability), not an entrance price. Choices "a", "b" and "c"

are incorrect, per the above Explanation: .

NEW QUESTION # 74

Which of the following assumptions means that money is the common denominator of economic activity

and provides an appropriate basis for accounting measurement and analysis?

- A. Going concern.

- B. Periodicity.

- C. Monetary unit.

- D. Economic entity.

Answer: C

Explanation:

Choice "c" is correct. The monetary unit assumption means that money is the common denominator for

economic activity and provides an appropriate basis for accounting measurements and analysis. Choice

"a" is incorrect. The going concern assumption has nothing to do with money per se. The going concern

assumption presumes that an entity will continue to operate in the foreseeable future. Choice "b" is

incorrect. The periodicity has nothing to do with money per se. The periodicity assumption is that

economic activity can be divided into meaningful time periods. Choice "d" is incorrect. The economic

entity assumption has nothing to do with money per se. The economic entity assumption is that economic

activity can be accounted for when considering an identifiable set of activities.

NEW QUESTION # 75

The effect of a change in accounting principle that is inseparable from the effect of a change in accounting

estimate should be reported:

- A. As a component of income from continuing operations, in the period of change and future periods if the

change affects both. - B. As a separate disclosure after income from continuing operations, in the period of change and future

periods if the change affects both. - C. By restating the financial statements of all prior periods presented.

- D. As a correction of an error.

Answer: A

Explanation:

Choice "c" is correct. A change in accounting principle that is inseparable from a change in accounting

estimate should now be reported as a change in estimate and thus as a component of income from

continuing operations, in the period of change and future periods if the change affects both. Distinguishing

between a change in accounting principle and a change in accounting estimate is sometimes difficult. For

example, a company may change from deferring and amortizing a cost to recording it as an expense

when incurred because future benefits of the cost have become doubtful. The new accounting method is

adopted, therefore, in partial or complete recognition of the change in estimated future benefits. The effect

of the change in principle is inseparable from the effect of the change in estimate. Changes of this type

are often related to the continuing process of obtaining additional information and revising estimates and

are therefore considered as changes in estimates. Choice "a" is incorrect. Restating the financial

statements of all prior periods would be done in the case of prior period adjustments (corrections of

errors), changes in accounting principle (retrospective application), and changes in accounting entity

(retrospective application). Choice "b" is incorrect. Correction of an error would be treated as a prior

period adjustment. Choice "d" is incorrect. Separate disclosure after income from continuing operations

would be done in the case of extraordinary items or discontinued operations. However, this disclosure

would not be made "in the period of change and future periods if the change affects both" but only in the

period of the extraordinary item or discontinued operation.

NEW QUESTION # 76

Gown, Inc. sold a warehouse and used the proceeds to acquire a new warehouse. The excess of the

proceeds over the carrying amount of the warehouse sold should be reported as a(an):

- A. Gain from discontinued operations, net of income taxes.

- B. Extraordinary gain, net of income taxes.

- C. Part of continuing operations.

- D. Reduction of the cost of the new warehouse.

Answer: C

Explanation:

Choice "b" is correct. Part of continuing operations.

Rule: When a fixed asset is sold, gain or loss is recognized as part of income from continuing operations.

The amount of the gain or loss is equal to the difference between the proceeds from the sale and the

carrying amount (FMV) of the fixed asset sold.

Choice "a" is incorrect. The gain is not extraordinary and is shown gross - not net of tax.

Choice "c" is incorrect. The gain is part of continuing operations - not discontinued operations.

Choice "d" is incorrect. The gain is not reported as a reduction of the cost of the new warehouse.

NEW QUESTION # 77

The cumulative effect of a change in accounting estimate should be shown separately:

- A. On the income statement above income from continuing operations.

- B. It should not be recorded separately on any financial statement.

- C. On the income statement after income from continuing operations and before extraordinary items.

- D. On the retained earnings statement as an adjustment to the beginning balance.

Answer: B

Explanation:

Choice "d" is correct. A change in estimate is handled prospectively. No cumulative effect adjustment is

made and no separate line item presentation is made on any financial statement. If a material change is

being made, appropriate footnote disclosure is necessary.

Choices "a", "b", and "c" are incorrect, per the above Explanation: .

NEW QUESTION # 78

The summary of significant accounting policies should disclose the:

- A. Concentration of credit risk of all financial instruments by geographical region.

- B. Criteria for determining which investments are treated as cash equivalents.

- C. Maturity dates of noncurrent debts.

- D. Terms for convertible debt to be exchanged for common stock.

Answer: B

Explanation:

Choice "d" is correct. The criteria for determining which investments are treated as cash equivalents

would be part of the summary of significant accounting policies. Choice "a" is incorrect. The maturity

dates of noncurrent debts are required disclosures, but are not a part of the summary of significant

accounting policies. Choice "b" is incorrect. The terms for convertible debt to be exchanged for common

stock are not accounting policies; they would be disclosed separately. Choice "c" is incorrect. The

concentration of credit risk of all financial instruments by geographic region may be a required segment

disclosure, especially for financial institutions. However, it would not be a part of the summary of

significant accounting policies.

NEW QUESTION # 79

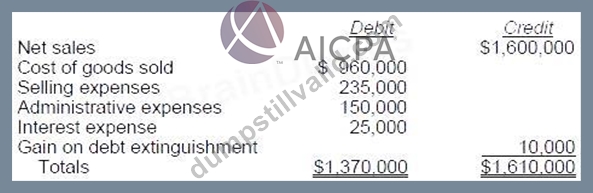

Coffey Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as

follows: Coffey's income tax rate is 30%. The gain on debt extinguishment is considered a usual and

recurring part of Coffey's operations. Coffey prepares a multiple-step income statement for 1988.

Income from operations before income tax is:

- A. $230,000

- B. $240,000

- C. $200,000

- D. $190,000

Answer: B

Explanation:

Choice "d" is correct. $240,000 The gain on debt extinguishment does not meet the unusual and

infrequent criteria of APB 30 to be treated as an extraordinary item (per SFAS No. 145, extinguishments

of debt are no longer automatically extraordinary), so it is included as part of income from continuing

operations.

NEW QUESTION # 80

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment

required for these transactions. These treatments are:

. Cumulative effect approach - Include the cumulative effect of the adjustment resulting from the

accounting change or error correction in the 1993 financial statements, and do not restate the 1992

financial statements.

. Retroactive or retrospective restatement approach - Restate the 1992 financial statements and adjust

1 992 beginning retained earnings if the error or change affects a period prior to 1992.

. Prospective approach - Report 1993 and future financial statements on the new basis but do not restate

1 992 financial statements.

During 1993, Quo increased its investment in Worth, Inc. from a 10% interest, purchased in 1992, to 30%,

and acquired a seat on Worth's board of directors. As a result of its increased investment, Quo changed

its method of accounting for investment in Worth, Inc. from the cost method to the equity method.

List B

- A. Cumulative effect approach.

- B. Prospective approach.

- C. Retroactive or retrospective restatement approach.

Answer: C

Explanation:

Choice "B" is correct. The equity method of accounting is applied retroactively when the investor has

acquired 20% ownership. Prior to acquiring the ability to influence the investee, the cost method is proper.

The retroactive restatement approach does not mean that this change is the correction of an error (which

is now treated retroactively), a change in accounting principle (which is now treated retrospectively), or a

change in accounting entity (which is now treated retrospectively). It just means that retroactive

restatement is the proper treatment.

NEW QUESTION # 81

During a period when an enterprise is under the direction of a particular management, its financial

statements will directly provide information about:

- A. Neither enterprise performance nor management performance.

- B. Both enterprise performance and management performance.

- C. Management performance but not directly provide information about enterprise performance.

- D. Enterprise performance but not directly provide information about management performance.

Answer: D

Explanation:

Choice "c" is correct. Financial reporting, and especially financial statements, usually cannot and do not

separate management performance from enterprise performance. Financial reporting provides

information about an enterprise during a period when it was under the direction of a particular

management but does not directly provide information about that management's performance. SFAC 1

para. 53

NEW QUESTION # 82

In 1992, hail damaged several of Toncan Co.'s vans. Hailstorms had frequently inflicted similar damage to

Toncan's vans. Over the years, Toncan had saved money by not buying hail insurance and either paying

for repairs, or selling damaged vans and then replacing them. In 1992, the damaged vans were sold for

less than their carrying amount. How should the hail damage cost be reported in Toncan's 1992 financial

statements?

- A. The expected average hail damage loss in continuing operations, with no separate disclosure.

- B. The actual 1992 hail damage loss in continuing operations, with no separate disclosure.

- C. The expected average hail damage loss in continuing operations, with separate disclosure.

- D. The actual 1992 hail damage loss as an extraordinary loss, net of income taxes.

Answer: B

Explanation:

Choice "b" is correct. Actual hail damage must be reported. Since the hailstorms are frequent, the

damage is not considered an extraordinary gain/loss. Thus, the damages would be shown in continuing

operations. No separate disclosure is necessary since hail damage is a common occurrence. Choice "a"

is incorrect. Hailstorms are not unusual and infrequent so the loss could not be classified as extraordinary.

APB 30 para. 20 Choice "c" is incorrect. Actual hail damage must be reported. Estimated hail damage

may be probable but is not estimable; so it should not be included in income calculations. Choice "d" is

incorrect. Estimated hail damage may be probable but is not estimable; so it should not be included in

income calculations.

NEW QUESTION # 83

Which of the following statements is incorrect regarding the inputs that can be used to measure fair

value?

I. Level I inputs are the most reliable fair value measurements and Level III inputs are the least reliable.

II. Level I measurements are quoted prices in active markets for identical or similar assets or liabilities.

III. A fair value measurement based on management assumptions only (no market data) would not be

acceptable per GAAP.

IV. The level in the fair value hierarchy of a fair value measurement is determined by the level of the

highest level significant input.

- A. I, II, IV.

- B. II, III, IV.

- C. I only.

- D. I, II, III, IV.

Answer: B

Explanation:

Choice "c" is correct. Statement I is correct and statements II, III, and IV are incorrect. Statement II is

incorrect because Level I measurements are quoted prices in active markets for identical assets or

liabilities only. Quoted prices in active markets for similar assets or liabilities are Level II inputs. Statement

III is incorrect because a fair value measurement based on management assumptions only is a Level III

measurement and is acceptable when there are no Level I or Level II inputs or when undo cost or effort is

required to obtain Level I or Level II inputs. Statement IV is incorrect because the level in the fair value

hierarchy of a fair value measurement is determined by the level of the lowest level significant input.

NEW QUESTION # 84

According to the FASB conceptual framework, predictive value is an ingredient of:

- A. Option A

- B. Option C

- C. Option D

- D. Option B

Answer: C

Explanation:

Choice "d" is correct. Yes - No. Predictive value is an ingredient of relevance but not of reliability.

Memorize:

Bud's relevance to "PFT."

Bud's reliability to "VRN."

NEW QUESTION # 85

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these

transactions as: a change in accounting principle, a change in accounting estimate, a correction of an

error in previously presented financial statements, or neither an accounting change nor an accounting

error.

Item to Be Answered

Quo changed from FIFO to average cost to account for its raw materials and work in process inventories.

List A (Select one)

- A. Change in accounting estimate.

- B. Neither an accounting change nor an accounting error.

- C. Change in accounting principal.

- D. Correction of an error in previously presented financial statements.

Answer: C

Explanation:

Choice "a" is correct. Change in inventory pricing method from FIFO to average cost is a change in

accounting principle.

NEW QUESTION # 86

A segment of Ace Inc. was discontinued during 1992. Ace's loss from discontinued operations should not:

- A. Exclude operating losses from the date the decision to dispose of the segment was made until the end

of 1992. - B. Include employee relocation costs associated with the decision to dispose.

- C. Include operating losses of the current period up to the date the decision to dispose of the segment

was made. - D. Include additional pension costs associated with the decision to dispose.

Answer: A

Explanation:

Choice "b" is correct. Ace's loss on discontinued operations should not exclude operating losses from the

date the decision to dispose of the segment was made until the end of 1992. All 1992 operating losses

should be included.

Choice "a" is incorrect. Employee relocation costs associated with the decision to dispose should be

included in the loss from discontinued operations.

Choice "c" is incorrect. Additional pension costs associated with the decision to dispose should be

included in the loss from discontinued operations.

Choice "d" is incorrect. Ace's loss on discontinued operations should include operating losses of the

current period up to the date the decision to dispose of the segment was made and also after that date.

All 1992 operating losses should be included.

NEW QUESTION # 87

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with

Quo's president and outside accountants, made changes in accounting policies, corrected several errors

dating from 1992 and before, and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these

transactions as: a change in accounting principle, a change in accounting estimate, a correction of an

error in previously presented financial statements, or neither an accounting change nor an accounting

error.

Item to Be Answered

Quo changed from LIFO to FIFO to account for its finished goods inventory.

List A (Select one)

- A. Change in accounting estimate.

- B. Neither an accounting change nor an accounting error.

- C. Change in accounting principal.

- D. Correction of an error in previously presented financial statements.

Answer: C

Explanation:

Choice "a" is correct. Change from LIFO to FIFO is a change in accounting principle.

NEW QUESTION # 88

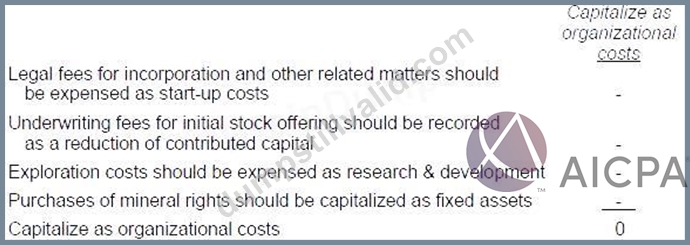

Tanker Oil Co., a development stage enterprise, incurred the following costs during its first year of

operations:

Tanker had no revenue during its first year of operation. What amount may Tanker capitalize as

organizational costs?

- A. $55,000

- B. $0

- C. $95,000

- D. $115,000

Answer: B

Explanation:

Choice "d" is correct. $0.

All organizational costs (start-up costs) should be expensed when incurred (per SOP 98-5).

NEW QUESTION # 89

......

Sep-2025 Latest DumpStillValid FAR Exam Dumps with PDF and Exam Engine: https://www.dumpstillvalid.com/FAR-prep4sure-review.html